The Family is a strategic, minority, long-term shareholder. We grow a portfolio of investments in scalable companies, ideally from an early stage so as to create a privileged relationship with their founders. We identify the best of the best, finding Entrepreneurs through a process based on content and education. We then work with founders, providing them with resources (education, unfair advantages, and capital) and maximizing their chance of large-scale success. In other words, we operate our own proprietary ecosystem, designed to defeat toxic startup environments and to build scalable businesses.

‘Ecosystem’:

the problem is that the very term has become a bit of a cliché.

Everyone uses it. For most people, its meaning has been lost along the

way. It has become irritating to hear everyone talking about the damned

‘ecosystem’, all the more so because in reality it’s often not an

ecosystem but a toxic environment for startups. And yet, if we follow Wikipedia, it seems that ‘ecosystem’ is a relevant word when it comes to describing the entrepreneurial environment. An ecosystem is

“A community of living organisms in conjunction with the nonliving components of their environment (things like air, water and mineral soil), interacting as a system.”

In

short, an ecosystem designates entities living together in a habitat.

It should be clear that those entities live better, longer, and happier

lives if that habitat is healthy!

Most

discussions regarding the best habitat for Entrepreneurs focus on

Silicon Valley. An abundant, mostly American, literature is dedicated to

analyzing Silicon Valley’s success on the entrepreneurial front. Some explain why everything is so good in the Valley

today, but don’t reveal how it all came together. Others go back to a

distant past, but jump to premature conclusions: everything happened

because of (you choose) Defense contracts / a mild climate in the Bay

Area / Stanford University / technology clusters / the culture of rewarding failure / favorable tax and legal conditions. Finally, many sources help understand the critical role played by certain individuals: Frederick Terman, Georges Doriot (even though he was on the East Coast), Robert Noyce, Andy Grove, or Steve Jobs.

It is worth noting, however, that most authors on the subject

rightfully conclude that history never repeats itself and therefore that

it’s not possible to emulate Silicon Valley’s story.

It’s

high time we went beyond simplistic analyses. There’s not much time

left: Silicon Valley is pulling way ahead and windows of opportunities

are closing fast for other territories. But at the same time, there is a

better understanding of how to grow a healthy entrepreneurial habitat: Steve Blank, Vivek Wadhwa (who recently joined TheFamily’s board), Paul Graham and Brad Feld are all getting a feel for what led to Silicon Valley’s dominance. Based on this understanding, it’s TheFamily’s mission

to protect ambitious Entrepreneurs against toxic environments and to

deploy our own proprietary ecosystem that maximizes their probability of

success. For that reason, we constantly work on understanding what

makes a great ecosystem and how it can be improved for the Entrepreneurs

who inhabit it. We’ve read a lot, met hundreds of people, and worked on

a model to make it easier to share our views on that matter.

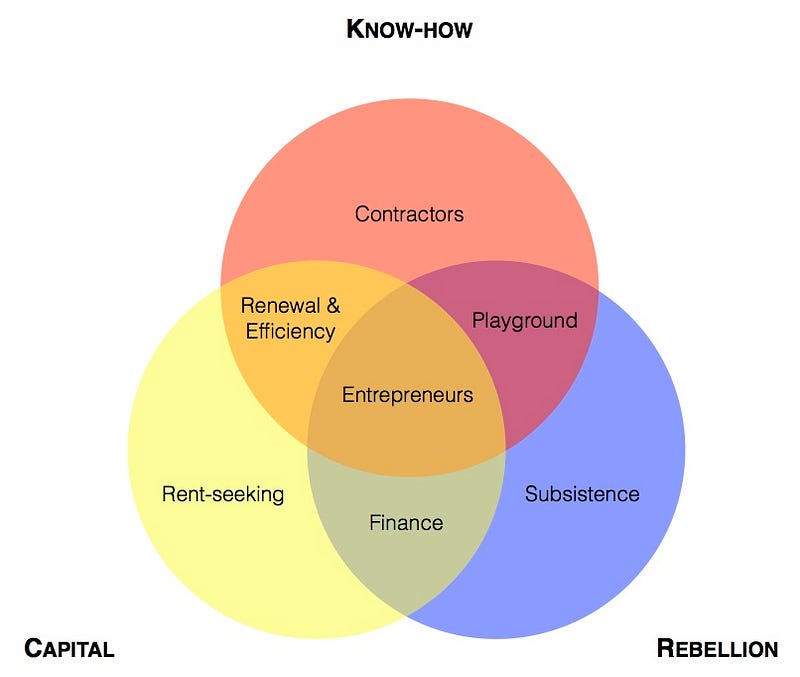

Three ingredients

Our

model is relatively simple, based on the idea that the entrepreneurial

ecosystem has three characteristic ingredients. They are as follows:

- capital—by definition, no new business can be launched without money and relevant infrastructures (which consist of capital tied up in tangible assets);

- know-how—you need engineers, developers, designers, salespeople: all those whose skills are necessary for launching and growing innovative businesses;

- rebellion—an entrepreneur always challenges the status quo. If they wanted to play by the book, they would innovate within big, established companies, where they would be better paid and would have access to more resources.

All

three ingredients are present, in variable proportions, in every

country. But the most important thing is not simply their relative

presence or absence in a certain place. Rather, it’s the degree to which

they mix within the entrepreneurial part of the economy. That is to

say, is there a place where all three ingredients come together, where

capitalists, engineers, and rebels get to know one another and do great

work together?

Seven combinations

The

way the three ingredients are combined tells a great deal about a given

country’s specific economy and sociology. There are seven possible

combinations.

Capital only = rent-seeking economy.

Oil-rich countries, such as those in the Persian Gulf, or those who own

an essential, sought-after infrastructure (such as the Panama Canal or

the pyramids in Egypt) are a good example of rent-seeking economies.

Those are often dominated by real estate, natural resources, and

utilities. In such economies, know-how is not rewarded (if it exists at

all) and rebellion is repressed, sometimes through violence.

Rent-seeking may also involve lots of lawyers: lobbying the government and suing innovative Entrepreneurs are simply two ways of seeking rent in democratic countries.

Capital + know-how = efficiency economy.

When capital meets know-how in the absence of rebellion, innovation

tends to be concentrated in established companies, which have only two

goals: renew their products and improve the efficiency of their

operations. As noted by Clayton Christensen,

these kinds of innovation destroy jobs and free up capital (rather than

empowering innovation which ties up capital and creates lots of jobs).

Freed capital is then invested elsewhere, often sustaining the

rent-seeking part of the economy. Above all, as noted by William Janeway,

efficiency is the enemy of innovation: you can’t expect radical,

Silicon Valley-style innovation from an economy without rebellion.

Know-how only = contractor economy.

It’s quite simple: if there are lots of engineers, but no capital to

invest and no taste for rebellion, then the best way to create value is

to sell the engineers' know-how to foreign companies. This is what India does:

selling IT engineering work to clients in developed countries. The

contractor economy is characterized by narrow margins (revealed by cost-plus, non-scalable business models), thus it doesn’t contribute much to economic development.

Know-how + rebellion = playground economy.

Why a playground? Because in such an economy, people may look like

Entrepreneurs when in fact they’re more like children without the right

(or the means) to grow. I have a specific example in mind. Every year or

so, I go back to my old engineering school in Brittany.

Every time I’m there, people tell me about lots of projects, whether in

research, business, or both. But once I leave, none of those projects

is ever heard from again. The following year, when I’m back on campus,

they’ve left no trace. Ideas and small-scale experiments simply fall

away into the ether. Why? Because when the economy lacks capital, local

rebels are unable to go from fleshing out an idea to building an empire.

The playground economy is a bit as if Larry Page and Sergey Brin had

invented PageRank, published their famous article,

tested the algorithm on the Stanford campus, then moved on to business

as usual because the banker refused them the loan they needed to start a

company. The playground economy exists where research is entrapped in

the academic world, or startups are prevented from growing due to

hostile regulations and a lack of capital. Playground innovation is

mostly funded by the government, through research grants or SMB subsidies. It creates few jobs (except for those managing government subsidies) and doesn’t create value at a larger scale.

Rebellion only = subsistence economy.

When there’s neither capital nor know-how to start and grow companies,

rebellion finds other ways: political movements, social activism,

artistic creation, and crime. Marginal artists in Berlin, punks in

England, and social activists in Porto Alegre are primary examples of

what dominates a subsistence economy. It gives birth to great art, it

drives social and political changes, it certainly stirs up anger, but it

doesn’t help build great business empires. An economy fueled only by

rebellion resembles many of the least developed countries: know-how is

scarce due to the failure of the higher-education system or massive

talent emigration; capital is spirited away by a fearful elite. Those

who stay are the people in need who just try to make ends meet;

charitable NGOs try to help them out; merchants make a business out of

scarcity and extract the residual value out of a failed economy. Indeed,

the only ones who create value in such economies are usually

rent-seeking merchants and illegal organizations. As a result, there may

be lots of capital, but since it’s been extracted

by predators such as traffickers or monopolist traders, it can’t be

invested into entrepreneurial ventures. As for genuine creators, they

fall into two categories: artists and activists. The former find success

abroad and are the local heroes; the latter ultimately trigger

revolutions. It should be noticed that subsistence economies are not

confined to developing nations: in every high income country, there are

areas where there is nothing but rebellion. I’m sure you can picture

them.

Rebellion + capital = financial economy.

Contrary to what people usually expect, finance is one of the most

rebellious sectors out there. Decades of deregulation of financial

markets have revealed how powerful finance is when it comes to forcing

change upon companies or even whole societies. Without the know-how to

start and grow a company, you can still make your mark (and earn a

bundle) by exerting your sense of rebellion in the financial sector. In

fact, many financiers are all the more rebellious as they come from

humble backgrounds and desperately want to escape their direct,

traumatic experience of the subsistence economy. A financial economy

captures a great deal of value and creates a great deal of wealth. But

the essence of the financial business does not lead to inclusive

institutions: as it is concentrated in the hands of the few, it makes it

complicated to ignite widespread economic development. A few rich

traders won’t make a flourishing economy!

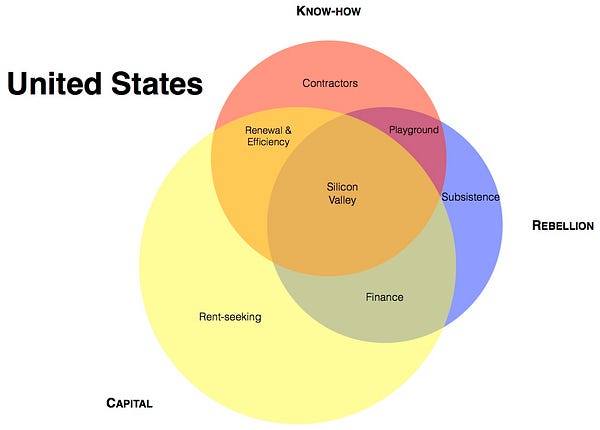

Capital + know-how + rebellion = entrepreneurial economy.

The Valley is the most obvious example. Capital initially came from the

Department of Defense, then from early venture capital funds, and now

from more traditional investors such as Goldman Sachs.

Know-how was present from the late 1940s on, thanks to the attraction

of engineers in the field of microwaves, then semiconductors. Finally,

rebellion is a mindset that is typical in California. Many rebels have gathered there, from the first motorcycle clubs to artists, hippies, student leaders, LSD advocates, gay activists, Ronald Reagan, and of course computer scientists. The Valley is the byproduct of those three ingredients mixing together.

A

quick step back, though. Is an entrepreneurial economy preferable? Is

creating a healthy habitat for Entrepreneurs really that important?

Aren’t we better off seeking rent or supporting the efficiency

innovation efforts of established companies? These are tricky questions,

but for us at TheFamily, the answers to them are clear: yes, yes, and

no, we’re not!

In an economy in transition,

an entrepreneurial economy creates far more value, more widely

distributed, than any other economy: in Silicon Valley, you’ll find the

headquarters of giant tech companies, ultra-rich Entrepreneurs,

thousands of highly-paid engineers, designers, and managers, an adjacent

economy that provides local services and amenities and creates lots of

jobs for the less educated, and massive tax revenues to finance better

public services. Silicon Valley is probably the closest to what Edmund

Phelps (Nobel Prize in Economics) calls “mass flourishing”:

Flourishing is the successful exercise of creativity and talents. To flourish, people have to engage a world of challenges and opportunities. The economy’s dynamism and the resulting experience of business life are central to our well-being.

Yet Silicon Valley has its weaknesses as well, demonstrated by the tension in its real estate market and, like elsewhere in the U.S., its limited social safety net.

These features should not be discounted as we look around at other

geographic areas and other economies where entrepreneurship can thrive.

The entropy in the system

It

is interesting to think about how a territory can drift from one

economy to another. There’s actually a lot of entropy in the system:

without successful Entrepreneurs, any entrepreneurial economy tends to

decline into something else. After all, Paris used to be a fantastically

entrepreneurial place at the dawn of the twentieth century. Hence the importance of immigration

in sustaining an entrepreneurial ecosystem: once entrepreneurial

institutions have been built by the first generation, it is vital that

Entrepreneurs from outside flow in to sustain the ecosystem and help it

grow.

Even

when you only have two ingredients out of three, entropy is still at

work and one of the two tends to be eradicated in time. Consider the

three scenarios below.

A playground economy (know-how + rebellion) turning into a subsistence economy (rebellion only).

If the know-how disappears, the playground is destroyed and there’s

only rebellion left. That’s what happened when Soviet Russia (which was

in itself a type of giant playground: lots of high technology, but no

business empires whatsoever) transitioned to capitalist Russia, as most

of the country’s know-how took off for Israel or the United States. From

that point on, money was to be made only from natural resources (hence a

rent-seeking economy dominated by oligarchs) until the prices went down

(to a subsistence economy without much hope for anyone).

A playground economy (know-how + rebellion) turning into a contractor economy (know-how only).

Even if they don’t leave the country, ultimately engineers get fed up

with failed projects trapped in the playgrounds. For them, it takes only

one step to become contractors. This is precisely the reason why every

French startup aims at becoming the next Google and ends up becoming a

small IT service business or Web agency. It’s OK, it pays the bills, but

margins are thin and it doesn’t scale—at

all. These startups-turned-Web-agencies don’t add up to an

entrepreneurial economy, they contribute to developing a contractor

economy with very little innovation.

A financial economy (capital + rebellion) turning into a subsistence economy (rebellion only).

Watch out when capital flees from a country without know-how: Greece is

a case in point. I suppose the United Kingdom also saw it coming in

2008. That is probably the reason why they decided to get serious about

growing an entrepreneurial ecosystem in the wake of the crisis.

It

isn’t enough to have two or even all of the key ingredients in one

place. They tend to not mix together too easily. Even worse, in many

cases they tend to evict one another, thus breaking the dynamics that

could make a non-entrepreneurial economy more entrepreneurial. We all

understand that it is much easier to seek rent, become a contractor or

stay in the playground. You have to work hard to counter that trend and

force the ingredients to mix together.

For

instance, you can try to turn a rent-seeking economy (capital only)

into a financial economy (capital + rebellion). Dubai or Abu Dhabi are

attempting to do just that, because when the oil reserves dry out,

rent-seeking will take a huge blow. Opening a Sorbonne subsidiary or

using the Louvre brand is probably their attempt to inspire some

rebellion and pave the way to the United Emirates becoming an

entrepreneurial place in a distant future. We’ll see.

The key role of Entrepreneurs

So

in order to counter that entropy, to mix all three ingredients and tie

them together in the long term, it takes, well, an entrepreneurial

ecosystem. And the only ones able to build it are—you guessed right—the

Entrepreneurs themselves, those whom Babak Nivi defines as having “the ability to serve a customer at the highest level of quality and scale, simultaneously”.

They initiate the best practices, overcome the obstacles and finally

build the institutions that become the pillars of an entrepreneurial

economy.

Consider the three cases that follow.

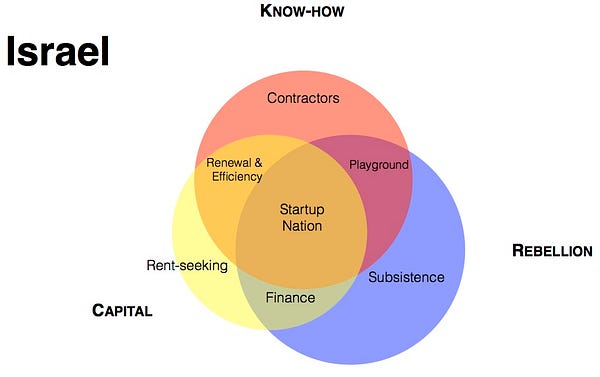

A playground economy turning into an entrepreneurial economy. It happened in Israel. The book Startup Nation

tells us about those Israeli aspiring Entrepreneurs who, in the 1980s,

built superb products but failed to market them to would-be customers.

They weren’t short in know-how (even less so after the collapse of the

Soviet Union, which brought many top-notch scientists to Israel), nor

were they short in rebellion (what with the famous chutzpah and all). But there was no capital: Israel was a playground economy at that time. Then, working with the Entrepreneurs, the Israeli government designed the Yozma

program to attract American venture capital and turn Israel into an

entrepreneurial ecosystem. Everything changed from that point on.

A financial economy turning into an entrepreneurial economy.

Here, we have London. The British government has a very simple

reasoning: if London is the European capital of the financial sector,

then it should become the European capital of innovation and technology

in the financial sector. The first « FinTech » Entrepreneurs benefited

from favorable conditions in the City (an economy already specialized in

finance and with a great deal of capital), then attracted talent from all over the European Union,

thanks to a very welcoming immigration policy towards citizens of other

member states. London already had quite a high level of capital and

rebellion (after all, England is home to the punk movement). The first

Entrepreneurs, supported by the government, did what had to be done to

overcome the deficit in know-how.

An efficiency economy turning into an entrepreneurial economy. This happened at the dawn of the Silicon Valley. Did you know that Fairchild Semiconductor,

the company that became both the matrix of the modern Silicon Valley

and an inspiring precedent for all its Entrepreneurs, was a subsidiary

of an established East Coast company called Fairchild Camera and

Instrument? At one point, Robert Noyce and Gordon Moore couldn’t stand

the constraints imposed by their corporate parent (which clearly favored

efficiency above entrepreneurship) and decided to leave and start

Intel. Their own personal touch of rebellion was enough to transform the

local ecosystem and give birth to the fastest-growing entrepreneurial

economy in the world.

In

each case, a virtuous circle was initiated. In Israel, the combination

of know-how and rebellion attracted foreign capital, with a little help

from the government. In London, capital itself helped buy know-how

thanks to the freedom of circulation in the European Union. What is

probably more difficult to ignite is rebellion, which really depends on

courageous, pioneering individuals who bear all the risks where

entrepreneurial institutions are still lacking.

The

idea that it takes Entrepreneurs to create an entrepreneurial ecosystem

sounds like a tautology. Yet we must continue to hammer on this point.

Many initiatives to create an entrepreneurial economy in the past came

from the government or big established corporations. As Josh Lerner proved in a remarkable book,

every one of those initiatives fell through (I insist: systematically,

in every case, without exception, at a 100% rate, this led to a

failure). In none of these cases did the government or established

companies manage to create an entrepreneurial economy by using a

methodical and planned approach. (In France, Sophia-Antipolis

is a case in point, as are all the later efforts to artificially create

such clusters.) This is the reason why you have to rely on the

Entrepreneurs and stimulate their ambition at the highest level

possible.

There’s an empirical law here, one that Brad Feld formalized in his 'Boulder Thesis' and one that also inspired us to start TheFamily: only Entrepreneurs

who combine long-term vision with short-term flexibility can inspire

and grow an entrepreneurial economy. If you have the ingredients, let

the Entrepreneurs cook them! That is precisely when heterogeneous

elements can mash themselves into a system, built by Entrepreneurs for

Entrepreneurs.

It

should be noted that an entrepreneurial economy takes off more easily

where other parts of the economy are not so strong. It’s difficult to be

contrarian where a certain type of value creation is at its strongest.

You can’t beat the financial economy in New York, but you can beat it in

California, with government contracts covering the build-up. Even Michael Milken had to be in California

to invent and implement high-yield bonds! London may be an exception

here—providing radical financial innovation at the heart of the

financial sector in Europe— but the success of the London FinTech sector

has yet to be proven and what’s more, ensuring it takes the active

support of the government because finance is a highly regulated sector

(yes, it is).

Also,

make no mistake: everybody likes to be called an Entrepreneur, because

there’s now a lot of prestige that comes with the title. But you’re no

Entrepreneur if you lack ambition, abide by the status quo, or don’t

want to build an empire. So it’s not enough to have people who call

themselves ‘Entrepreneurs’. Docile engineers, however competent, make

bad hackers. Complacent capitalists prefer to seek rent rather than to finance risky new ventures. What you need are those whom Marc Andreessen calls “imperial, will-to-power people who want to crush their competition.”

Walter

White, the ultimate rebel, summed it up for us: he’s not in the meth

business (= know-how), nor in the money business (= capital), but in the

empire business (= all of the above + rebellion).

Benchmarking different countries

Another

interesting perspective is found by looking at various countries and

trying to understand why some perform better than others when it comes

to growing a healthy entrepreneurial ecosystem.

Let us begin with the United States. The ingredients are there: fantastic amounts of capital + lots of know-how + a great potential for rebellion (at least since 1776). The rent-seeking economy is obviously a huge part of the American economy, with oil, real estate, and utilities:

wherever there is a lot of capital, people tend to seek rent.

Fortunately, know-how is there as a counterbalance and is heavily

represented within the entrepreneurial economy, especially in Silicon

Valley. The financial economy is also huge (New York, Dallas, Chicago),

but is receding as compared to Silicon Valley, which is attracting

capital and even becoming a political power in the American democracy.

Israel

is a very interesting case, as it used to have a serious gap: capital.

The Yozma program helped launch a very dynamic local venture capital

ecosystem, even though traditional small businesses still had

difficulties accessing capital in the Israeli banking system. Hence in

the Israeli economy, available capital has been primarily invested in

entrepreneurial ventures, not traditional businesses. As a result, the

Israeli entrepreneurial economy now attracts most of the know-how and

diminishes the contractor part of the economy: contrary to their Indian

(or French) counterparts, Israeli engineers work for Israeli startups

(and the American tech companies that buy them) instead of working as contractors for foreign clients.

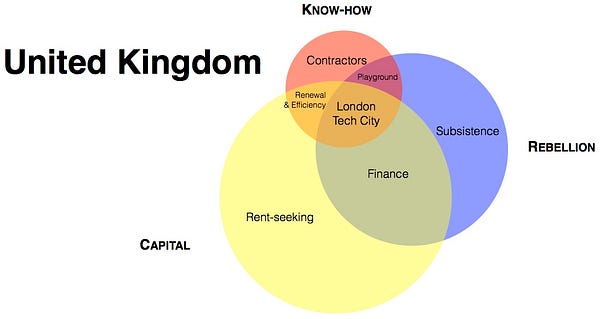

The United Kingdom

is another very interesting example. In short, the British economy

accounts for an enormous amount of capital, divided between a massive

rent-seeking economy (notably in real estate) and a very dynamic

financial economy. Lack of know-how explained why it was so difficult to

create an entrepreneurial economy. But this has been overcome thanks to

freedom of circulation in the European Union, the goal of making a

FinTech capital out of London and aggressive support from both

governmental and financial regulators. Contrary to most of their counterparts, the British government often sides with the rebels instead of siding with the rent-seekers.

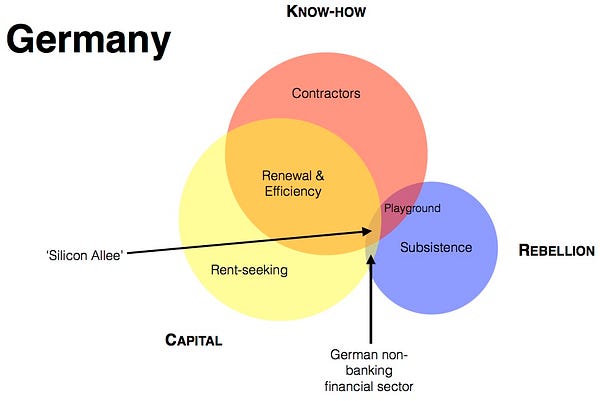

Germany

is the land of efficiency. There is a lot of know-how in Germany,

including that coming from neighboring Eastern European countries. But

venture capital is small, probably due to the activism of German banks

and their tradition of financing businesses. As a consequence, know-how

is mostly “trapped” in established companies and allocated to

efficiency innovation within big German corporations. Since they

practice continuous innovation, those corporate powers tend to be ahead

of their counterparts in other countries; but this does not amount to

entrepreneurial innovation (I’ll spare you the VW jokes). Having worked

in the German business world, I can tell you: there is no rebellion

there. The entrepreneurial economy is thus confined in the marginal Berlin culture, and since capital and know-how are retained by established companies, the German entrepreneurial economy is far from thriving.

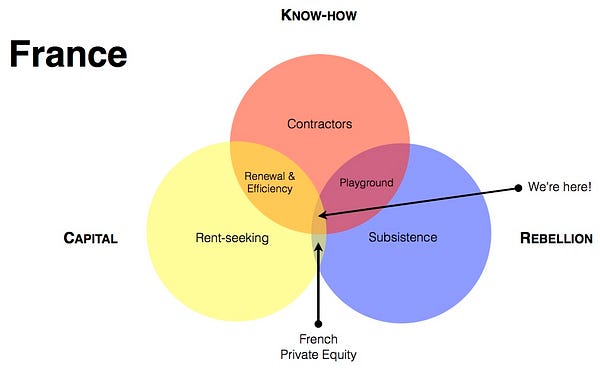

Let us conclude with the French

case—also an interesting one, if only because it inspired us to start

TheFamily. My partners and I often speak about the toxicity of the

French environment for Entrepreneurs. We have founded TheFamily to try

to battle this toxicity.

The

model detailed above allows us to better understand where the French

toxicity comes from. After all, France is an enigma: why do we have such

a hard time building great entrepreneurial ventures when we have so

much capital, know-how and rebellion? Every year, many people leave

traditional companies to start their own venture. Know-how is abundant:

our engineering schools are among the best in the world, as demonstrated

by American companies that locate their R&D operations in France. Finally, there appears to be capital to finance launching and growing tech startups: venture capital key metrics are up; and they say all promising companies manage to raise capital in Paris.

And

yet, it doesn’t work. Why? The short answer goes like this: in France,

no one mixes up the three ingredients. Capitalists, engineers and rebels

are there, but they don’t live in the same world and are often openly

defiant towards one another.

The longer version follows three main arguments.

There’s a lot of capital in France, but the rent-seeking economy is so powerful (real estate, taxi companies,

pharmacists, lawyers, doctors, craftsmen, farmers, solicitors and

clerks of all sorts) that capitalists see no reason why they should risk

anything by investing in startups. A lot of capital is also tied up in

heavy infrastructures (transportation, energy, telecommunications,

tourism), but that capital is also captured by special interests that

seek rent (in tourism) or confine their innovation efforts to renewal

and efficiency (telcos). The only rebels in French capitalism are those

in the private equity sector, who frighten many stakeholders with

aggressive leveraged buyouts. Even venture capitalists stay in line in

France, as their funds are mostly financed by the Government through Bpifrance.

There’s a lot of know-how in France,

but everything is done so that it is mostly allocated to efficiency or

contractor work. France has good engineers, but there are two problems.

1) As Gwendal Simon explains here,

French engineers are usually not interested in execution. They were the

best students throughout their time in school, so they see themselves

as corporate executives, not software developers. 2) Thanks to our

research tax credit, a matter of national pride, engineers' salaries are

subsidized by the government (yes: those engineers that every tech

company is willing to pay good money for are subsidized in France). As a

result, the engineering job market works like a cartel: every company,

whether in the efficiency, playground or contractor economy, can afford

to pay the same (relatively good) salary, whatever value they create. It

is thus difficult for entrepreneurial ventures with no capital to match

those salaries and to attract the best engineers.

Finally, there’s a lot of rebellion in France, as demonstrated by frequent strikes and shirts being torn off corporate executives.

But when that rebellion comes from Entrepreneurs trying to make their

way out of the playground, it attracts nothing but problems:

cease-and-desist orders, lawsuits, even nights in prison. It should be

said again and again: in every country, Entrepreneurs usually don’t fit

in the box. Only in some select countries, such as the U.S., rebellion

allies itself with know-how and capital to overcome obstacles and beat corporatism.

In France, on the other hand, rebellion is tolerated, even supported,

but not in entrepreneurial matters. As a result, it thrives in other

universes, such as activism or art creation. But Entrepreneurs are

confined to the playground.

My

own perception, after many years spent in that ecosystem, is that

France fails on the entrepreneurial front because entrepreneurship is

suppressed by both rent-seeking (which ties up available capital),

contracting (which captures know-how), and corporatism (which suppresses

rebellion). It is not a caricature, but the inconvenient truth: we’re a

mix of Tunisia (for tourism), London (for the real estate market), India (for IT services) and Greece (for the political system ready to explode).

Where

is our entrepreneurial economy? For sure, there are a lot of

Entrepreneurs in France, and they create hundreds of startups. A

worrying sign, however, is that none of the currently dominant tech

companies has grown out of France. This is why we’ve worked hard at

TheFamily on finding ways to connect know-how, rebellion and capital

enough to help promising ventures grow and scale.

France’s

entrepreneurial economy is already proud of BlaBlaCar, en route to a

dominant position on the global long-distance ride-sharing market: lots

of know-how, lots of capital (thanks to foreign investors), and a good

amount of rebellion.

But

there are other promising jewels in the crown, notably future global

players currently growing within TheFamily’s own ecosystem. Save, a company that rescues all your smartphones and tablets,

was founded less than two years ago: it will have 700 employees and a

€2M monthly revenue by the end of this year; in 2016, it will launch in

the U.S. and China, adding to the 7 countries in which it is already

operating. Algolia, another company in our portfolio, offers a Hosted Search API; it was also founded in 2013, raised $18M a few months ago

and will soon have crossed the threshold of 250 billion API calls from

customers all over the world. Out of 350 companies in our portfolio, we

believe that we now have more than 50 such promising stars.

This

is what we do as a long term, strategic, minority shareholder: operate

our own ecosystem, empower Entrepreneurs, defeat toxic environments, and

build new empires. So join up with us, and let’s get to work.

Here is a reading list I highly recommend for anyone willing to better understand entrepreneurial ecosystems:

- Marc Andreessen, “What It Will Take to Create the Next Great Silicon Valleys, Plural”

- Steve Blank, “The Secret History of Silicon Valley” (video + blog)

- Kim-Mai Cutler, “How Burrowing Owls Lead To Vomiting Anarchists (Or SF’s Housing Crisis Explained)”

- Paul Graham, “Can You Buy a Silicon Valley? Maybe”

- Paul Graham, “How To Be Silicon Valley?”

- Paul Graham, “Why Startups Condense in America”

- Jaron Lanier, “Early Computing’s Long, Strange Trip”

- Balaji Srinivasan, “Software is Reorganizing the World”

- Vivek Wadhwa, “Silicon Valley Can’t Be Copied”

A PBS program on Silicon Valley (you can watch it from the U.S. only).

For those willing to read more, a few excellent books by William Janeway, Josh Lerner, Enrico Moretti, Carlota Perez, AnnaLee Saxenian.

Source: https://medium.com/welcome-to-thefamily/what-makes-an-entrepreneurial-ecosystem-815f4e049804